Year End Tax Planning for Limited Company Directors: 5 April 2026 Checklist

Year end tax planning for limited company directors before 5 April 2026. Use this practical UK checklist to cut surprises and plan tax efficiently.

Year End Tax Planning for Limited Company Directors: 5 April 2026 Checklist

Year end tax planning for limited company directors is time-sensitive now, because 5 April 2026 is just weeks away. If you leave everything until the final few days of the tax year, you usually lose options. If you review your numbers in late February or March, you can still adjust salary, dividends, pension contributions, and spending timing in a legal, controlled way.

This guide is for owner-managed UK companies where the director is also a shareholder. We will keep it practical, use real numbers, and point you to official HMRC and GOV.UK pages so you can verify the details. Your exact position will depend on your wider income, family situation, and company profit profile, so treat this as planning guidance rather than one-size-fits-all advice.

Quick summary: before 5 April 2026, check your director pay mix, estimate dividend tax bands, review pension funding through the company, use available ISA and capital gains allowances where relevant, and make sure your bookkeeping is clean enough to support all of it.

If you want support with this before year end, we can run the numbers with you through our company accounts service, bookkeeping service, and Self Assessment support.

Why this year-end window matters more than most directors think

A lot of tax planning ideas only work if action is taken before 5 April. That includes using your ISA allowance, using your annual capital gains exempt amount, and deciding whether certain payments should land in this tax year or next. Once the date passes, you cannot backdate most of these decisions.

There is also a practical point. March and early April are busy for accountants and payroll teams. If records are late, payroll has errors, or dividends were never documented properly, even a good plan becomes hard to execute. Right, so speed matters, but clean records matter even more.

On top of that, many directors are now juggling personal tax, company tax, and digital reporting changes at the same time. The simplest way to stay in control is to work from a checklist with dates and figures, not from memory.

Key 2025 to 2026 figures to use in your planning

Use current published rates and allowances while planning, then confirm final numbers before filing.

| Item | 2025 to 2026 figure | Why it matters |

|---|---|---|

| Personal Allowance | £12,570 | Tax-free personal income limit in most cases |

| Basic rate band | £37,700 | Helps you plan salary and dividend tax bands |

| Higher rate threshold | £50,270 | Income above this moves into higher rates |

| Dividend allowance | £500 | First £500 of dividends is taxed at 0% rate band |

| Dividend tax rates | 8.75%, 33.75%, 39.35% | Rates depend on your tax band |

| ISA allowance | £20,000 | Personal tax-free investment wrapper |

| Pension annual allowance | £60,000 (subject to rules) | Core year-end pension planning lever |

| Capital gains annual exempt amount | £3,000 | Tax-free gains each tax year |

Official references:

- Income Tax rates and allowances

- Dividend Allowance factsheet

- ISA overview

- Pension annual allowance

- Capital Gains Tax annual exempt amount

Worth mentioning though, thresholds are only one part of the picture. National Insurance, student loan deductions, child benefit position, and your spouse or civil partner’s tax band can all shift the best route.

Year end tax planning for limited company directors: your March checklist

1) Reconcile bookkeeping and draft profits first

Planning without accurate bookkeeping is guesswork. Start by reconciling bank accounts, checking director loan postings, and confirming expenses are coded correctly. If profit is overstated, you may hold back dividends you could have taken. If profit is understated, you may overpay dividends and create problems with unlawful distributions.

At this stage we normally ask directors three direct questions:

- What profit do you expect before Corporation Tax?

- What have you already paid yourself as salary and dividends?

- Do you expect any one-off income or costs before year end?

If those answers are uncertain, fix that first. You can only plan tax properly once the base numbers are credible.

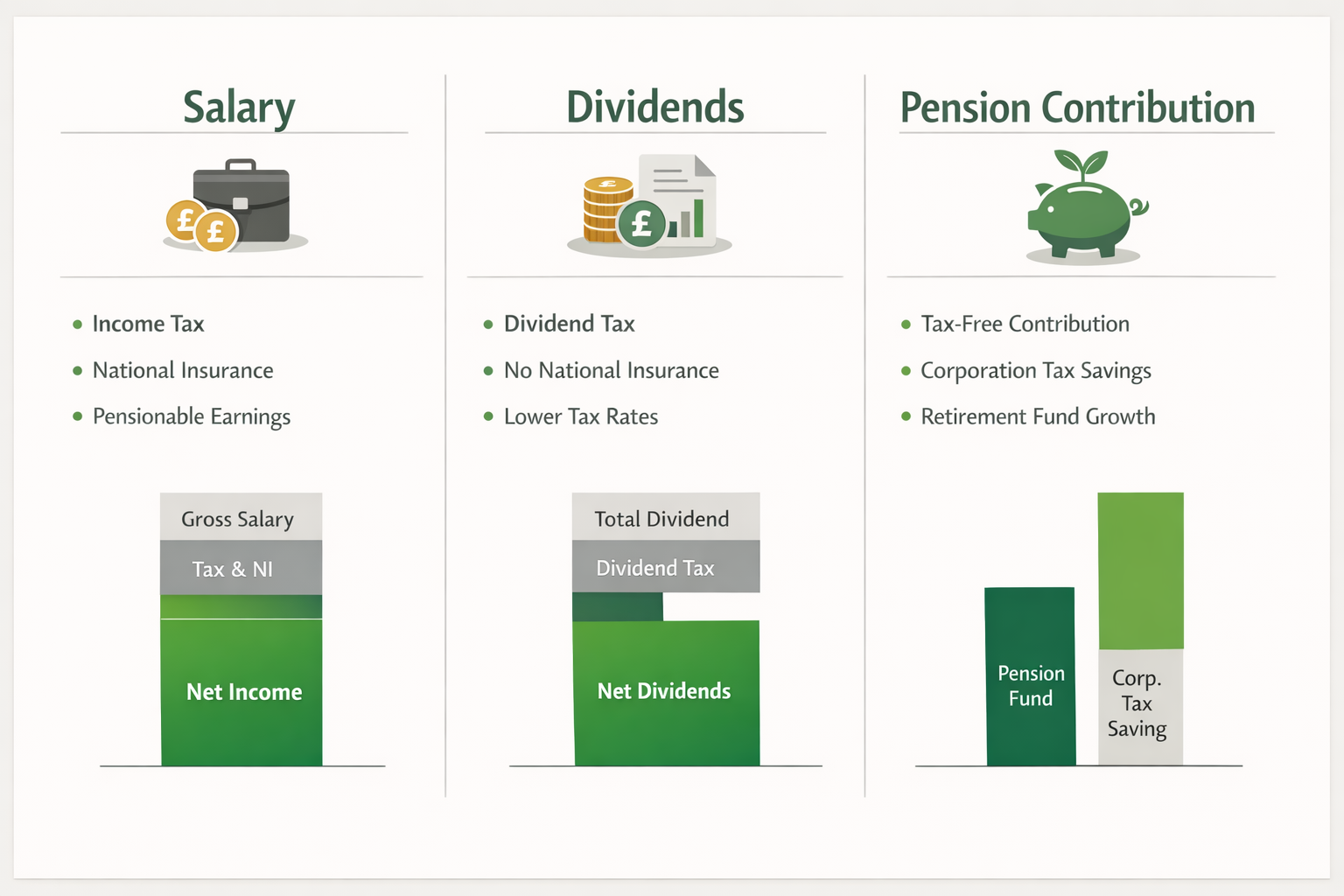

2) Review salary level and payroll setup

Many owner-directors keep salary around common thresholds and draw the rest as dividends. That can be sensible, but only if payroll is set correctly and submitted on time through RTI. Check that your year-to-date salary matches your intended plan and that no duplicate or missing payroll runs exist.

If you have employees, review employer National Insurance costs as part of this exercise too. Payroll decisions made in March often affect cash flow in April and May, not just tax.

3) Model dividends before declaring anything further

Dividends are not automatic tax savings. You need post-tax company profits available for distribution, and you need board minutes plus dividend vouchers in place. On the personal side, you need to know how much of your basic rate band is still unused.

Worked example 1: salary and dividends with current bands

Assume director Alex has:

- Salary in 2025 to 2026: £12,570

- Proposed dividends before 5 April 2026: £40,000

- No other personal income

How the dividends are taxed in principle:

- First £500 at dividend allowance rate: £0 tax

- Next £37,700 at 8.75%: £3,298.75

- Remaining £1,800 at 33.75%: £607.50

Estimated dividend tax total: £3,906.25

If Alex declared £30,000 instead of £40,000, everything above the allowance would stay in the basic rate band and higher-rate dividend tax would not apply. That is why timing and amount both matter. Sometimes a smaller dividend now and another after 6 April is cleaner.

4) Consider company pension contributions before year end

Company pension contributions can be one of the most useful levers for directors because they may reduce Corporation Tax while building personal retirement savings. The rules are technical in places, especially around annual allowance, carry forward, and whether contributions are wholly and exclusively for business purposes, so this part should be reviewed case by case.

Worked example 2: pension contribution and Corporation Tax effect

Assume a company expects taxable profits of £120,000 before pension contribution and is within the main 25% Corporation Tax rate band.

If the company pays a £20,000 employer pension contribution for the director before year end, taxable profits could reduce to £100,000 (subject to deductibility rules).

Estimated Corporation Tax reduction:

- £20,000 x 25% = £5,000

That is a material difference, and it often helps directors who do not need extra personal drawings right now.

5) Use allowances that reset on 6 April

Some allowances are annual and disappear if unused.

- ISA allowance: up to £20,000 each tax year per eligible person.

- Capital gains annual exempt amount: £3,000 for individuals.

- Pension annual allowance: up to £60,000 in many cases, with important limits and taper rules for higher incomes.

Married couples and civil partners can often plan together, not because there is a special “family allowance”, but because each person has their own allowances and tax bands. Used properly, that can reduce the total household tax bill.

6) Review company purchases and timing of expenditure

If the business needs equipment anyway, timing can change when tax relief arrives. For plant and machinery purchases, Annual Investment Allowance can give 100% relief up to the limit, though eligibility and category of asset matter.

Worked example 3: equipment purchase before year end

Assume your company is considering buying new laptops and office kit costing £18,000. If bought and brought into use before year end, and assuming qualifying expenditure under AIA rules, taxable profit may reduce by £18,000.

If your Corporation Tax rate is 25%, that could reduce the tax bill by around:

- £18,000 x 25% = £4,500

If the purchase is delayed until after year end, relief may still be available, but in the next accounting period, which pushes the cash benefit back.

7) Check director loan account position before 5 April

Director loan accounts can become messy when personal spending is posted through the company or dividends are assumed but not formally declared. If the account is overdrawn, there can be tax consequences for the company and, in some cases, benefit-in-kind issues.

This is one of those areas where the rules get a bit fiddly. Do not rely on rough bookkeeping codes here. Reconcile the balance and agree a clean action plan before year end.

8) Put upcoming deadlines in your diary now

Year-end planning is not only about 5 April. The follow-on deadlines matter:

| Deadline | What it usually covers |

|---|---|

| 5 April 2026 | End of tax year for personal allowances and planning actions |

| 6 April 2026 | New tax year starts |

| 31 July 2026 | Second payment on account for 2025 to 2026 Self Assessment, where applicable |

| 31 January 2027 | Online Self Assessment filing and balancing payment for 2025 to 2026 |

HMRC deadline reference:

Common mistakes we see every March

Assuming dividends can be backdated

They generally cannot be backdated just to fit a tax plan. Dividends need proper paperwork and sufficient distributable profits at the time.

Ignoring personal tax when planning company drawings

Directors sometimes optimise for Corporation Tax and forget the personal side. A decision can look efficient inside the company and still create a larger personal tax bill than expected.

Leaving pension planning until April

If contribution timing is part of your strategy, waiting until after 5 April means you may miss this year’s allowance position.

Forgetting spouse or civil partner planning opportunities

Where shareholding and legal ownership are set up properly, household-level planning can be more efficient than planning each person in isolation.

No cash reserve for tax bills

Even a well-run business can get squeezed if all surplus cash is drawn out before known tax payments fall due. Keep enough headroom for Corporation Tax and personal tax commitments.

How this links to MTD and wider compliance in 2026

Even if this article is focused on year-end planning, the process you build now helps with wider compliance changes. Cleaner digital records, monthly reconciliations, and clearer separation of personal and company transactions reduce friction across everything, including annual accounts, VAT returns, payroll, and Self Assessment.

That said, do not overcomplicate it. A simple monthly routine beats a perfect system you never maintain.

If you want us to pressure-test your setup before 5 April, start with our contact page. We can review your numbers, map your options, and help you choose a plan that is practical for your business rather than theoretical.

FAQ: Year-end tax planning for limited company directors

What is the biggest tax planning action I should prioritise before 5 April 2026?

Start with accurate profit and drawings figures. Without that, decisions on dividends, pension contributions, or spending timing are usually wrong.

Should I always take a low salary and high dividends?

Not always. The right split depends on total income, National Insurance position, pension goals, and whether you need stable PAYE income for mortgage or finance applications.

Can my company pay into my pension and reduce Corporation Tax?

Often yes, if the contribution is allowable. The details depend on your circumstances and pension allowance position, so take tailored advice before finalising.

Is buying equipment before year end always tax efficient?

Only if the purchase is genuinely needed and qualifies for relief. Buying something unnecessary just for tax reasons is rarely a good business decision.

Do I need to file anything with HMRC on 5 April itself?

5 April is the tax year cut-off for many planning actions. Filing deadlines are later, but waiting until filing season usually removes planning choices you have now.

Final next step

Book a one-hour year-end review before mid-March and make decisions while there is still room to act. Bring your latest management figures, payroll summary, and dividend history. You will leave with a short action list and clear dates, which is far better than guessing in the final week.

About Golden Tree Consulting

Financial expert at Golden Tree Consulting

Helping businesses in Croydon navigate financial complexities with tailored solutions

More Articles You Might Like

Continue exploring our financial insights

MTD for Income Tax UK: April 2026 Checklist for Sole Traders and Landlords

MTD for Income Tax starts in April 2026 for many sole traders and landlords. Use this practical checklist to get ready, avoid penalties, and file with confidence.

Do I Need an Accountant for My Croydon Business?

Not sure if your Croydon business needs an accountant? Learn the difference between bookkeeping and accounting, and when it’s time to get professional help.

Why UK Startups Are Choosing Estonia for Company Formation

Explore why Estonia is ideal for UK startups. Learn how digital-first systems, zero corporate tax on retained profits, and fast company formation make Estonia a smart move for growth.